The client, a Private Credit Fund firm wanted the TresVista team to calculate the Fair Market Value (FMV) of the loans within their independently managed U.S. portfolio quarterly, based on their contractual terms and expected cash flows.

To perform a valuation of leveraged loans portfolio quarterly.

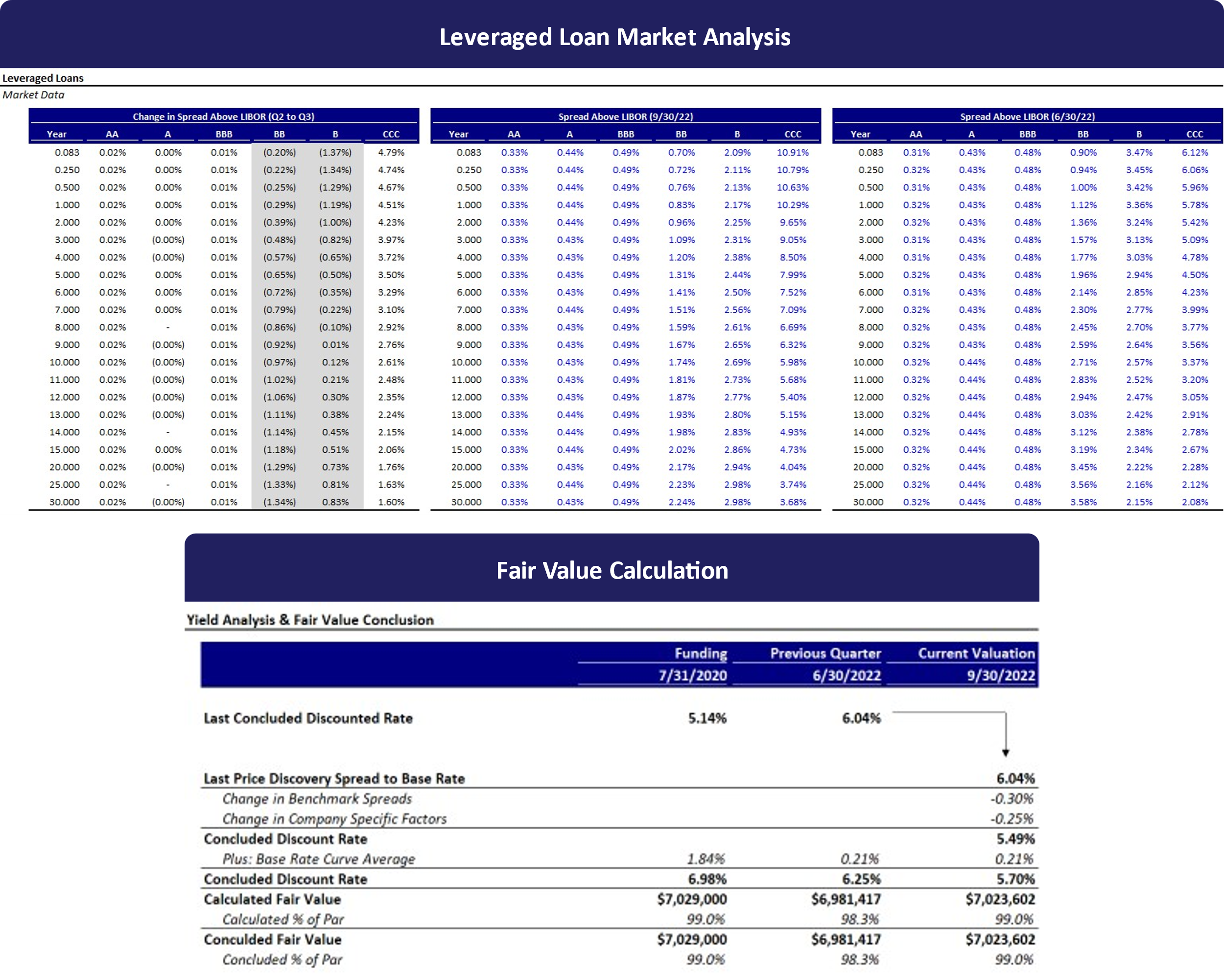

The TresVista team followed the following process:

• The team worked on a DCF model capturing all the cashflows which should then be discounted at the market rates

• Floating Base Rate: Forward curve of Base Rate as per the date of origination

• Setup Dates: As per the coupon and principal repayment frequency

• Cashflows: Interest from [Spreads + Base Rate] & Principal Amortization

• Initial Discount Rate: Goal Seek to get the implied YTM which gets the loan at par (i.e., 100%)

• Hence, the implied YTM (which may vary as per the market and financial conditions) is the WACC equivalent for the DCF analysis

The major hurdles faced by the TresVista team were calculating the original/initial discount rate (implied YTM) for the new loans and incorporating the impact of the market movements & company’s financial performance onto the existing discount rates.

The TresVista team gained a significant perspective on valuing a private credit loan and tracking its movement to the market. The deliverable assisted the client to track the performance of the fund quarter-on-quarter in relation to the market.