The client, a Private Equity firm, asked the TresVista team to conduct valuation of five subsidiaries (one public and four private) and eventually the holding company. The client provided the historical financial statements and based on different methods of valuation, they wanted the team to evaluate fair value of the subsidiaries and the holding.

To build valuation model for a downstream oil holding company and its subsidiaries.

The TresVista team followed the following process:

• Conducted research to study the impact of Russia Ukraine war and expected recession on the price of products sold by the company, keeping in mind government subsidies

• Prepared a revenue buildup for each subsidiary based on the product mix and forecasted the price and volume of each product

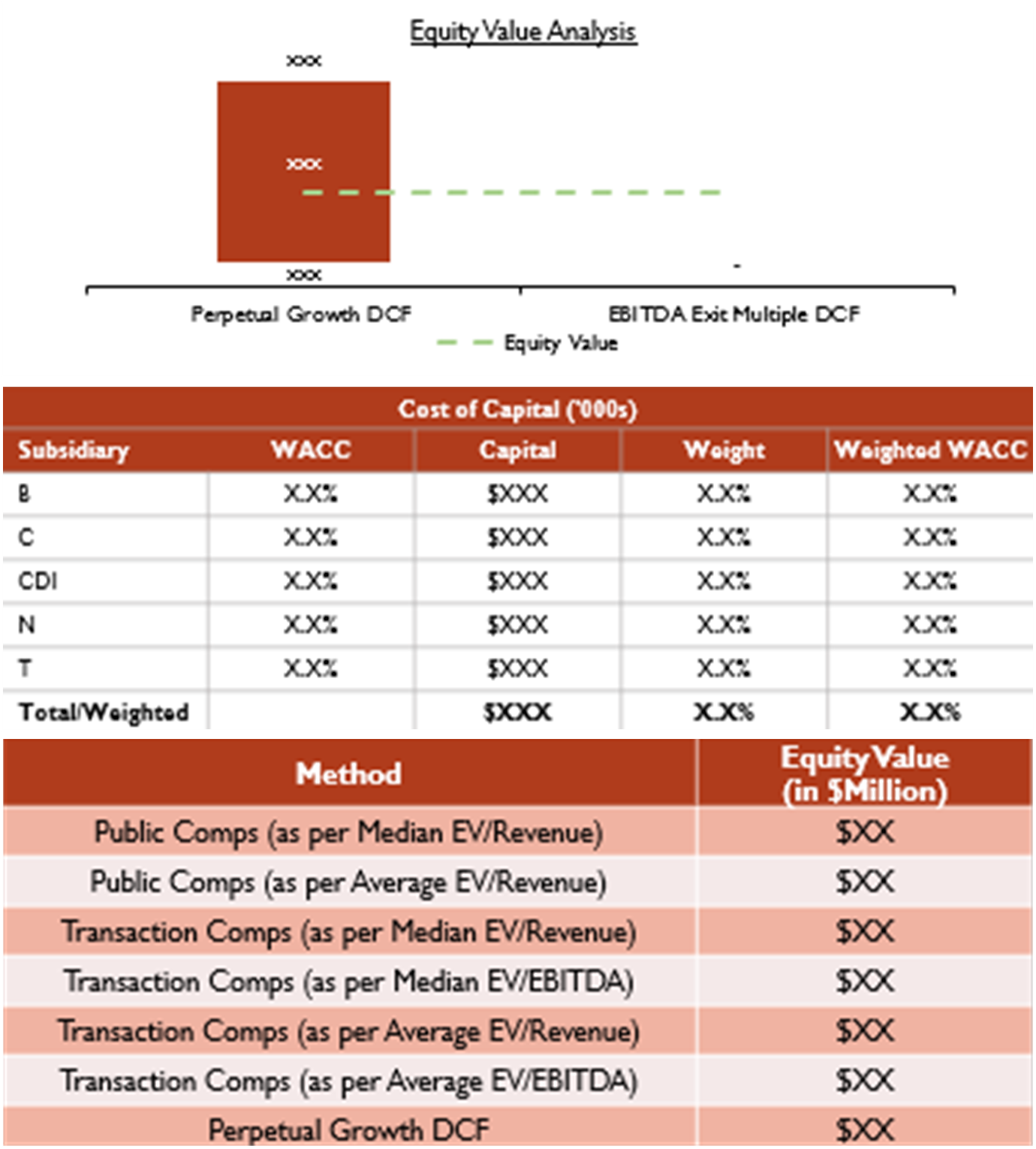

• Conducted valuation of each subsidiary based on the most suitable method, including DCF, book value, liquidation value, public and transaction comparables

• Holding company was valued by consolidating the financial statements of each subsidiary and discounting the cash flows using a blended Weighted Average Cost of Capital (WACC)

• A valuation report was prepared to summarize the valuation methodologies used and the assumptions made to forecast the financial statements

The major hurdles faced by the TresVista team were:

• Understanding the impact of subsidies and economic events on the price of fuel products

• Deciding the most suitable valuation method for each subsidiary based on the financial health

The team overcame these hurdles by researching about the budgeted subsidies and the impact of various events on the price of products. The team decided the valuation methods based on the financial health of the company keeping all the factors in mind.

The TresVista team proposed the idea of liquidation analysis to value the companies which cannot be valued as a going concern and provided the flexibility of “Revolver” to avoid negative cash balance. The team also created a template to account for inter-company transactions.